Profitable businesses go bankrupt every day. Usually while they're growing.

The Position

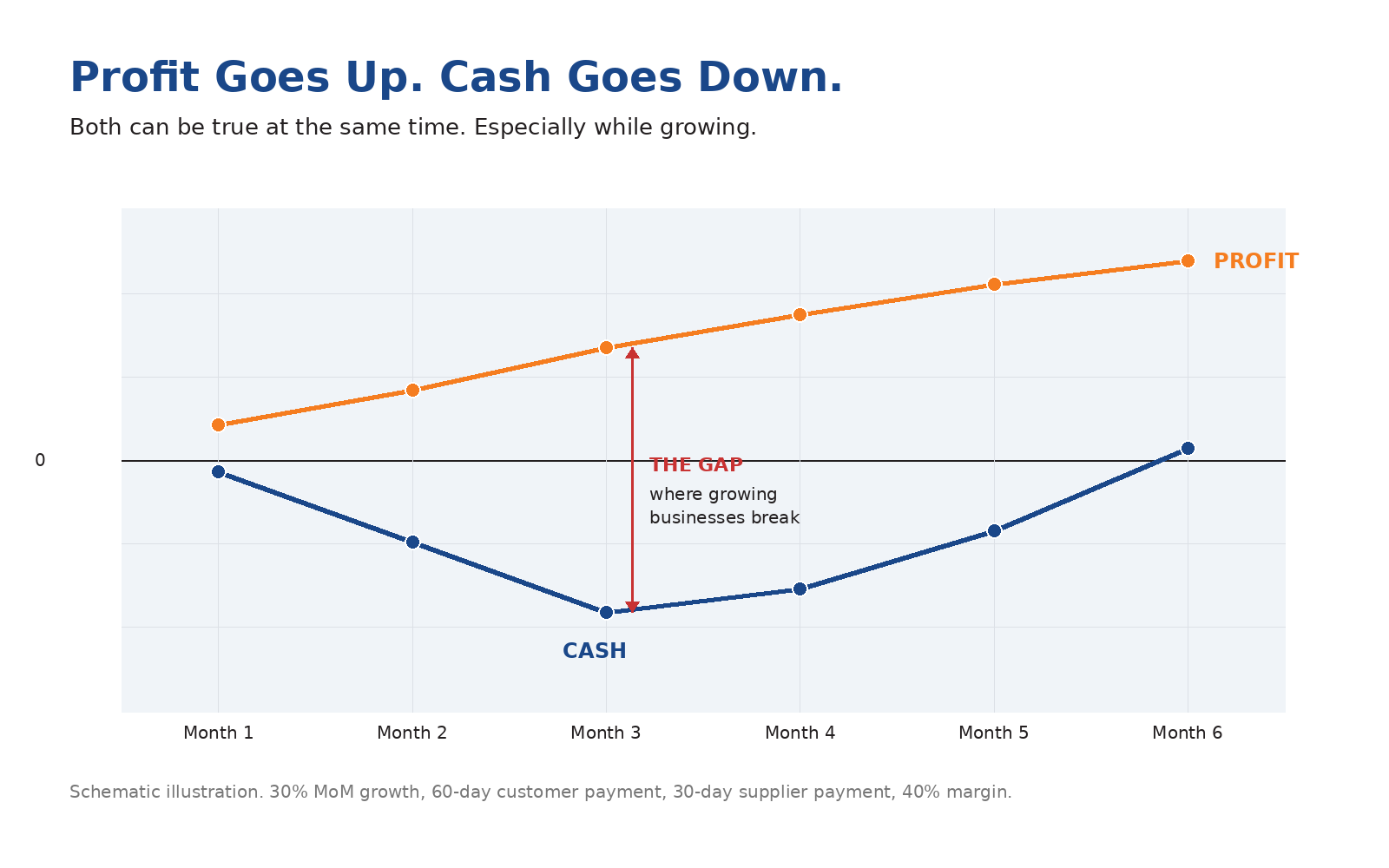

The fastest-growing SMEs in Southeast Asia are also the ones most likely to go bankrupt. Not because the business is bad. Not because the market turned. Because the founder watched a number on the profit-and-loss statement go up every month — and didn't notice the number in the bank account quietly moving the other way. Profit and cash are not the same thing. The gap between them is where growing businesses go to die.

The Problem Most SME Owners Don't See Coming

It starts the same way every time. The business is growing. New customers each month. Last quarter looked better than the one before. The accountant produces a profit-and-loss report and shows a healthy profit number — bigger than last year, bigger than the year before. The owner takes the report into Monday meetings and says, with reason, that things are going well.

Then a supplier calls about an overdue invoice. Then payroll comes around and the bank balance is somehow short. Then the owner stares at the bank line, the credit card statement, and the receivables ledger and starts to feel a kind of fear no profit number ever caused. How can the business be losing money when the P&L says it isn't?

It isn't losing money. The P&L is correct. The business is profitable. The business is also out of cash. Both can be true. Both usually are, somewhere in the trajectory of a growing SME.

Profit is yesterday's news. Cash flow is whether you survive the next 90 days.

The Reframe

The mistake is treating profit and cash as if they were the same thing. They are not. They measure different things over different timeframes, and confusing them is the most common reason healthy businesses die mid-growth.

Profit measures whether the work the business did was worth doing — whether revenue exceeded costs, on paper, over some accounting period. It is a historical statement. It tells the owner what was true between a start date and an end date that have already passed.

Cash measures whether the business has the money to meet its obligations today, tomorrow, next month. It is a forward-looking statement. It tells the owner what will be possible — or impossible — depending on what arrives and what leaves the bank account between now and the next critical payment.

Profit is yesterday's news. Cash flow is whether you survive the next ninety days.

The reason this distinction matters more for growing businesses is structural, not cosmetic. Growth requires capital to be deployed up front. Inventory bought before it sells. Staff hired before they generate revenue. Marketing spent before customers convert. All of it paid for now, recovered later — usually much later than the owner assumed when the spending decision was made. The faster the growth, the wider the gap between what the business has already earned on paper and what it actually has in the bank. A flat business with predictable cash conversion can survive on yesterday's profit logic. A growing business cannot.

The Three Questions

There is a discipline that prevents this. It is not complicated, it does not require a chief financial officer, and it can be done in fifteen minutes every Friday afternoon. It is three questions an owner runs against the business each week.

The first question is whether revenue is growing faster than cash. Most owners know whether revenue is up — it is the number they celebrate. Far fewer know what cash actually did in the same period. The way to check is brutal in its simplicity: compare the bank balance at the end of last month with the bank balance at the end of this month, after stripping out any new borrowing or capital injection. If revenue grew and the underlying cash position did not, the business is funding its own growth from somewhere — usually from the next period, which has not yet happened. That is fine if it is a deliberate strategic choice. It is dangerous if the owner did not notice it was happening.

The second question is how long it takes between making a sale and being paid for it. Accountants call this number Days Sales Outstanding, or DSO. It is the average number of days between issuing an invoice and receiving the money. For most SMEs in business-to-business markets, the answer is somewhere between thirty and ninety days. The number itself is less important than what happens to it as the business grows. If DSO stays the same while revenue triples, the amount of cash trapped in unpaid invoices triples too — and that is cash that cannot be used to pay suppliers, payroll, or rent. A growing business with a stable DSO has a cash gap that widens every month, automatically, by design.

The third question is how many weeks of cash runway the business has. Runway is cash on hand divided by weekly outflow — how long the business could survive if no new revenue came in tomorrow. It is the most important number in the business, and the one the fewest owners can answer without looking. Healthy runway depends on the industry, but a useful rule for SMEs is twelve weeks as a minimum, twenty-four weeks as comfortable. Below twelve weeks, the business is one bad month away from a crisis. Below six, the crisis has already started — the owner just has not seen it yet.

What This Actually Looks Like

To make this concrete, picture a business at one hundred thousand ringgit in monthly revenue, growing thirty per cent month-on-month. Gross margin is forty per cent. Customers pay in sixty days. Suppliers are paid in thirty. The business is profitable from day one — a healthy forty thousand ringgit monthly margin, and rising.

By month three, monthly revenue is one hundred and sixty-nine thousand ringgit. Cumulative profit on paper is one hundred and thirty thousand ringgit. The owner looks at the P&L and sees a business that has earned more in three months than it did in the previous full year. There is no reason to feel anything but optimistic.

The bank account tells a different story. Suppliers have been paid every month — sixty thousand, then seventy-eight, then a hundred and one thousand ringgit, each on a thirty-day cycle. But customer payments from month one only arrive in month three. Month two and month three revenue is still floating in receivables. The cash has not yet come in. By the end of month three, the business has paid out two hundred and thirty-nine thousand ringgit in cumulative outflows and received only one hundred thousand ringgit in cumulative inflows. The bank balance is short by one hundred and thirty-nine thousand ringgit — assuming the business started the period at zero. In reality, most growing SMEs do not.

The P&L says the business made one hundred and thirty thousand ringgit. The bank balance says the business owes one hundred and thirty-nine thousand. Both are correct. They are measuring different things.

What Survives Growth

This is not a corner case or a thought experiment. It is what growth does to any business whose owner only watches profit. The fix is not slower growth. The fix is wider visibility. Watch the cash line as carefully as the revenue line. Run the three questions every Friday. Know the runway number from memory.

The owners who survive growth are not the ones who got lucky with timing or who happened to have rich parents at the right moment. They are the ones who saw the gap forming, week by week, while there was still time to close it — to renegotiate supplier terms, to shorten DSO, to slow a hire, to draw a credit line before it was needed rather than after. Investors think in cash flow because that is what they are ultimately paying for: future cash. Operators who think the same way build more resilient businesses. The math is not different. The horizon is.