The half of the cap table most founders forget — and the 60/40 split that fixes it.

The Position

Most founders learn the same lesson the same way. They build a real business — late nights, sacrificed weekends, every customer earned the hard way — and at the end of three years they discover they own twenty per cent of it. The investor who wrote the cheque on day one owns the rest. There was no fraud. There was no betrayal. The cap table simply did what cap tables do — it counted money, not work. And the founder accepted the structure on day one because that is what every term sheet looks like, what every accountant draws, what every first round at the kitchen table with friends and family seems to require. The default is the trap. The fix is not refusing the investment. It is structuring it so the cap table measures both what was put in and what was done.

The Problem Most Founders Don't See

It usually begins with money. A founder has an idea and the conviction to chase it. The early conversations happen with what investor circles call the three Fs — friends, family, and people willing to back conviction without much else. They write the first cheque. Because the founder treats money as the constraint that matters most, the cheque buys a large share of the company. Sixty per cent. Sometimes eighty.

For the first year, no one notices the imbalance. The founder is everywhere — running sales, managing operations, training the team, fixing what breaks, making the decisions that turn a plan into a business. The investor waits for updates. Then the business turns its first real profit. One hundred thousand dollars on the bottom line, after a year of work that consumed the founder and barely touched the investor's calendar.

The cap table does its job. Eighty thousand dollars goes to the investor. Twenty thousand goes to the founder. Both outcomes are completely consistent with the equity structure agreed at day one. Both outcomes are also a recipe for the founder to feel — accurately — that the cap table is paying the wrong person.

Repeat that distribution for two or three more years, and the founder reaches a fork in the road that has no good option. Buy back the shares at a valuation now ten times the original cheque, or walk away from the business they built.

A cap table that counts only capital prices the business as if no one will need to build it.

The Reframe

The standard logic of equity treats the question as if there were only one input to the business: money. Capital comes in, the business comes out, ownership of the business gets shared in proportion to capital contributed. For passive investments — buying a share of a fund, or a slice of a building someone else is operating — this logic works. The capital is the input. There is no other input.

For an operating business that is being built rather than just funded, the logic breaks. A business is not a financial product that exists the moment money is deposited. It is a system that someone has to design, populate, manage, refine, and grow into something worth the original price paid for it. The capital is one input. The work that turns the capital into a functioning business is another input. Treating them as the same — collapsing both into the single category of money in — is the structural error.

The fix is not to refuse the investment. Founders need capital. Investors deserve protection for the capital they put at risk. The fix is to recognise that equity has two underlying sources of value and to split the cap table accordingly. Capital earns its share. Work earns its share. The two are accounted for separately because they are economically distinct.

The cap table that counts only capital prices the business as if no one will need to build it. The cap table that counts both starts the partnership with a structure that matches what is actually about to happen.

The 60/40 Framework

The framework that closes the gap is straightforward. Total equity is split into two layers.

Capital equity is sixty per cent of the total. It is the ownership earned by money put in. It is distributed proportionally between the parties who contributed capital. If a founder contributes twenty thousand dollars and an investor contributes eighty thousand, the founder's share of the capital equity layer is twenty per cent of sixty per cent, and the investor's share is eighty per cent of sixty per cent. The math is the same as the conventional cap table — but it now applies to only sixty per cent of the total ownership, not all of it.

Sweat equity is the remaining forty per cent. It is the ownership earned by the work of operating the business. It is distributed between the people who do the building. In most early-stage SMEs, that is the founder. Sometimes a working cofounder shares it. Sometimes a key early hire earns a portion through vesting. The structure is flexible, but the principle is fixed: whoever is doing the building owns a share of the building.

The split itself matters as much as the principle. Sixty per cent for capital and forty per cent for work is not a balanced compromise; it is a deliberate weighting that preserves the discipline of capital-first thinking while refusing to erase the operator. Investor protection still dominates the cap table — capital remains the larger share — and the investor is not being asked to subsidise effort that may not show up. But the operator's contribution is no longer zero on paper while being everything in practice. A fifty-fifty split would invite over-promising, because the operator's share would no longer reflect the capital provider's first claim on the upside. A seventy-thirty split would replicate the original problem at a smaller scale. Sixty-forty is the line that lets both parties live with the structure for the years it takes to make the business worth more than the day-one cheque.

The structure is also durable through later rounds. New capital coming in dilutes the capital layer proportionally; sweat equity dilutes only when new operators join. The principle survives growth.

What This Actually Looks Like

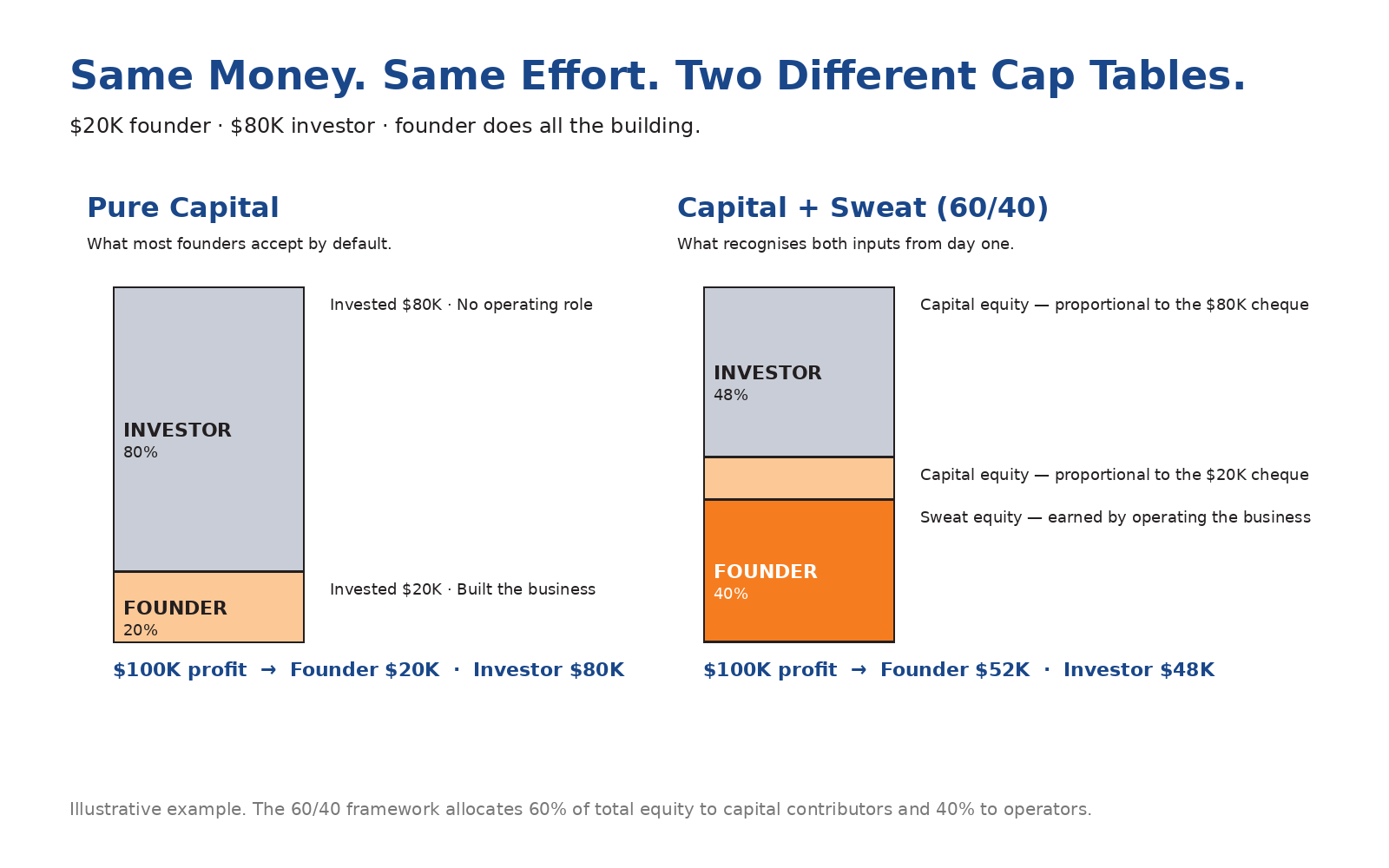

To make this concrete, return to the original numbers. The founder contributes twenty thousand dollars and assumes the full operating role. The investor contributes eighty thousand dollars and takes no operating role. The total capital raised is one hundred thousand. Under the 60/40 framework, the cap table looks like this:

In the capital equity layer, the founder earns twelve per cent and the investor earns forty-eight per cent. In the sweat equity layer, the founder earns the full forty per cent and the investor earns nothing. Final ownership: founder fifty-two per cent, investor forty-eight per cent.

The investor still holds a substantial stake — nearly half the company for a cheque that funded most of the capital. The founder, who is doing the building, holds the controlling share. When the business reaches its first hundred-thousand-dollar profit year, the distribution is no longer twenty-eighty. It is fifty-two thousand to the founder and forty-eight thousand to the investor.

Run that distribution for three years and the founder has earned a hundred and fifty-six thousand dollars from the business they built. Run the pure-capital structure across the same three years and the founder has earned sixty thousand. The difference is not a rounding error. It is the difference between a partnership that survives and one that collapses into resentment and buyout negotiations.

The math is the proof. The structure does not require new tools, new lawyers, or new vehicles. It only requires that the cap table be drawn to recognise both inputs from day one.

What Survives the Build

Cap-table structure is one of the few decisions a founder makes once and lives with forever. Refinancing is possible, buyouts are possible, restructuring is possible — but all of them are expensive corrections to a structural decision that could have been made correctly at the start. The reason most founders get this wrong is not naivety. It is the absence of any framework that treats sweat as worth structuring around. Investors think in deployed capital. Operators think in deployed effort. A cap table that recognises only one of those measures the business as if half of it does not exist. The 60/40 split is how to count both — from day one, before the work begins, while the conversation is still about how to build something worth the cheque.